5 min read

Solving the Guidance Puzzle: How Investors Can Get a Better Read on Management Guidance Using Alternative Data

Don Wood

CRO

Guidance matters, but needs a more sophisticated approach

With the increasing proliferation of alternative data use, many buy-side firms have become skilled at positioning into earnings. When calibrated correctly and executed with a variety of complementary data sources, investors can generate an accurate estimate of where a top-line KPI will hit. One area of softness with these tools has been guidance. But guidance for the future can often matter more for immediate stock volatility than beating or missing earnings estimates for the prior quarter. Given the high frequency and low latency of Alternative Data, investors can have a glimpse at how KPIs are trending just prior to an earnings call – similar to how economists think of “nowcasting” for economic indicators.

However, many investors use an overly simplistic approach to building a read on guidance. For companies that provide guidance (especially towards the latter half of the season), there has been a temptation to take the intra-quarter data points and to extrapolate an estimate of guidance in a linear fashion for the whole quarter. In theory, this allows the fund to not only position for a potential reported beat/miss, but also for the guide.

Admittedly, positioning into guidance is tough. Management has competing reasons to guide, including tempering expectations or reinforcing a narrative. A surprise guide can change the earnings reaction, regardless of how accurate one’s positioning was into the prior quarter’s print. Based on our discussion with a wide cohort of fundamental managers, many take the data they’ve collected and linearly extrapolate to project a guide.

Building a more nuanced, data-driven approach to guidance

Our analysis suggests that this can be improved on. To do so, we built Pre-Cast, a guidance model which balances simplicity with a need for accuracy that investors can rely on. Pre-Cast anticipates upcoming vendor data up to six months out, helping guide expectations around potential forward looking guidance revisions by management teams. It incorporates things that management likely focuses on like seasonal patterns, as well as shorter-term inflections and changes that may be a function of strategy, new product, or a rapidly changing environment. To do so, we incorporate vast datasets across multiple years to develop a confident 180-day extrapolation of the performance indicator in question.

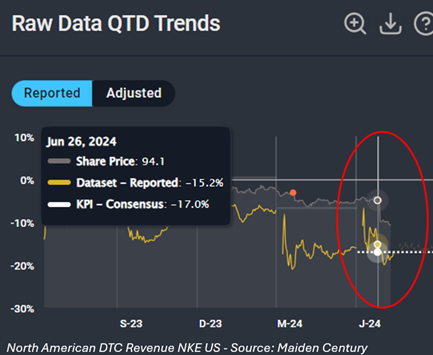

The proof is in the pudding. Our Pre-Cast forecast generates accurate estimates vs. consensus, allowing our users to incorporate the potential for a guide surprise into their earnings positioning. Let’s take Nike (NKE US) as a topical example. In its most recent quarter, Nike reported a “dim forecast”, sending its shares down 20%, their worst one-day response since the founding of the firm.

The swirling consternation around the storied shoe wear and fitness apparel company has to do with the business realignment being executed by its new CEO, John Donahue. In order to combat the decline in sales for its most popular shoes (such as the Air Force 1s and Air Max), Nike initiated a strategy to restrict supply and “regain pricing power.” Our datasets quickly identified significant deterioration in North American DTC sales, a strategy emphasis for the brand.

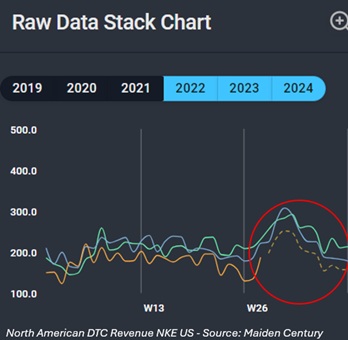

Positioning for that guide not only required investors to understand this deterioration, but to understand it within the historical context of prior seasonality, a factor extremely important in apparel. In the chart below, with Pre-cast turned on, we can see the clear decline in the spending trend vs the prior two calendar years, even when adjusting for seasonality.

By incorporating seasonality and the signs of short-term inflection/change, this model outperforms guidance extrapolation of the limited intra-quarter sample sets, giving investors a better shot at positioning into a guidance surprise.

How does this work for your names? Find out in a live demo: contact us.